Inflation and supply chain issues have driven up the cost of just about everything lately, including car payments, groceries, and the price of energy. With the highest inflation rates since the early 1980s, most consumers are now spending more money on the basic necessities of modern life than ever before.

With homeowners pinching pennies to make ends meet, selling solar can be tricky. This is especially true because, along with inflation, interest rates have also risen. Gone (for now) are the days of zero-interest loans to finance those solar systems.

“We are moving at light speed from the lowest interest rate environment, I think, in any of our lifetimes to what is certainly the highest in decades,” explains Mike Gilroy, CEO of Sungage Financial.

But, none of this means that solar is no longer a great investment, of course. It’s just that the way we sell it has to acknowledge these facts. During our recent “Demystifying Solar Financing” panel at Empower, solar financing leaders from across the country laid out some winning strategies for selling solar in this high-interest rate environment.

Why are loan rates rising?

First, it’s important to understand why solar loan rates are rising. We often hear about interest rates going up, but what does that really mean? The Federal Funds Rate, at its most basic, is the cost of money.

“The Federal Funds Rate is the base borrowing cost,” explains Matt Murray, Chief Marketing Officer of Goodleap. “So, every bank is borrowing money overnight and then deciding ‘what do I need to do on top of that to make the money I need to to run a viable business?’”

When that rate is low — or even zero — financing companies can offer loans at lower rates, for example, the 0% car and solar loans that were so popular in 2020 and 2021.

“In that low-rate environment, it was natural that the industry gravitated toward low, fixed APRs. I think the 0%, 25-year loan was the epitome of that,” Mike says.

As the rate rises, the cost of capital for financing companies increases. This is why we’re now seeing loans more in the 5-6% range and greater. If the Federal Funds Rate continues to rise, we can expect the interest rates customers pay to do the same.

Again, though, none of this means that solar isn’t a great investment for homeowners. So, let’s get to the strategies.

Highlight utility rate increases

There’s an old saying: All you can count on is death, taxes, and utility companies raising rates. (Or something like that.)

This continues to be true. The US Energy Information Administration (EIA) determined in its short-term energy report, “The US residential price of electricity will average 14.9 cents per kilowatt hour in 2022, up 8% from 2021.” The agency projects electricity costs will go higher still in 2023.

Of course, to many of us, 14.9 cents sounds pretty cheap for a kWh. You can check out your specific region on this chart. Spoiler alert: No matter where you’re located, the price of electricity has gone up, and will very likely continue to go up.

So, even though a solar loan may be a bit more costly than it was in times with lower interest rates, its value could arguably be even greater when compared to the rising prices of energy overall.

There are a couple questions you can use to bring this home with homeowners:

- “How has your electric bill changed in the past couple years?” Of course, many customers won’t have their bills from the past couple years, so bring the utility-rate data with you. Then extrapolate out over the life of the system; many customers will be surprised. (Aurora can do this for you automatically.)

- “How long do you think it will take you to break even?” With many financing options (see below for a specific one) a system can still be cash-flow positive almost instantly, and payback times are often less than the homeowner would guess.

Make sure homeowners know about solar incentives

While many homeowners are understandably focused on interest rates and inflation, it’s important to let them know that there are also forces making the end cost of solar cheaper.

Chief among these is the Inflation Reduction Act (IRA). Among other great things, it extends the Solar Investment Tax Credit (ITC) out to 2032, and restores it to its original 30% value. (The ITC was slated to drop to 23% in 2023, and 10% for commercial only in 2024.)

“[The IRA] may be the public works project of our lifetime, and it’s thrilling to see how people are beginning to apply it,” John Bumgarner, General Manager of Solar and Storage for Sungage.

So, while interest rates and inflation are currently high, with an uncertain future, one thing is certain: The ITC isn’t going anywhere. And, when you balance higher interest rates with the higher ITC, solar is actually less expensive for many homeowners than when the ITC was scheduled to wind down.

Focus on financing options that do make sense

While interest rates may be high, there are still incentives you can use to make loans more appealing. For example, no money down.

“You can still use the 0 down, 0 out of pocket — customers love that,” Matt says. “Whenever you can say nothing out of pocket, no fees, none of that, people get excited about that.”

Putting no money down also makes the cash flow equation that much clearer. While the Day 1 payment savings might not be as compelling as a homeowner wants, with utility rates constantly rising, switching the focus to lifetime savings and short payback times still shows substantial return on investment.

“Rather than leading with the APR,” Mike explains, “you can look at total lifetime savings as a way to frame the opportunity and the value.”

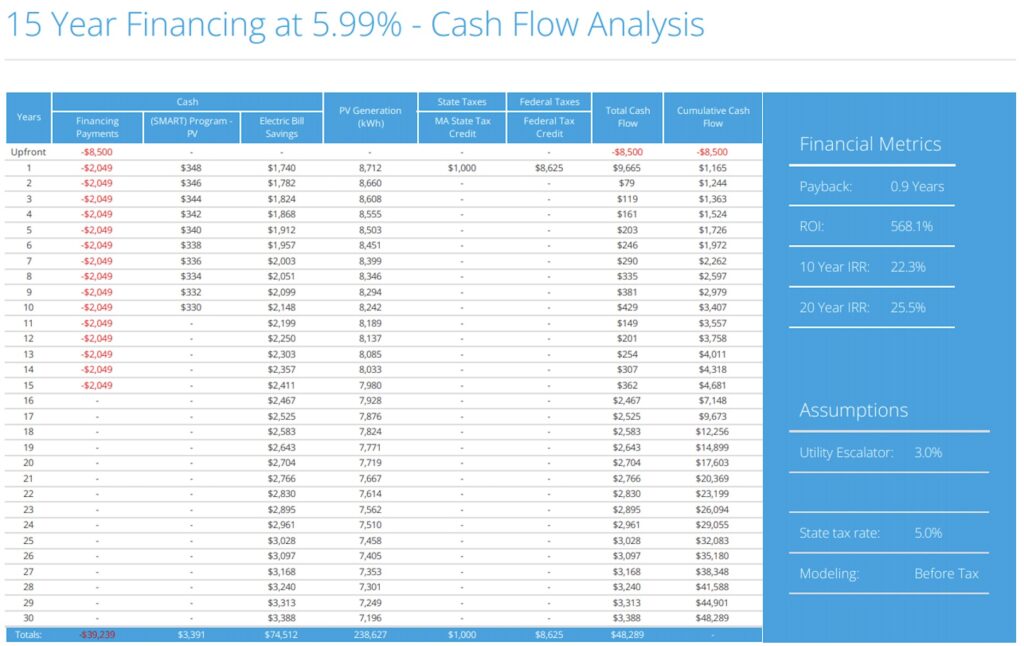

Here’s an example. This 8.4 kW solar system is financed at 5.99% for 15 years, with no money down. Cost is $28,750. There’s a state tax credit of $1,000 and the Federal Tax Credit comes to $8,625. For the first 10 years, the homeowner also gets SMART program payments based on how much energy they generate. The $8,500 upfront payment is payable over 12 months, and is covered by the rebates in year one.

This delivers a positive cumulative cash flow in a year. Yearly cash flow increases as utility rates rise, then jumps when the loan is paid off in 15 years.

Getting creative like this gives consumers more options, and truly highlights the value of solar.

“Talk more about annual savings that people are going to see over a period of time — repackaging things, just a little,” Matt concludes. “And then get out there and continue to talk about the incentives that are available for people, whether it be through the ITC at 30% or different state benefits… there are all kinds of incentives.”

How much do high interest rates really cost?

While it’s good to emphasize lifetime value in this time of high interest rates, some homeowners may still be uncomfortable. Here is a possible opportunity to show that high interest rates shouldn’t be a deal breaker. All other things equal, if the homeowner is financing $15,000 for a solar system for 15 years, the difference in payments isn’t as big as you might think:

- 6% = $127 per month

- 4% = $111 per month

- 2% = $97 per month

Of course every dollar counts, but many homeowners hear high interest rates and immediately shut down. But, a $30 per month difference between a 2% interest rate and a 6% interest rate doesn’t sound as scary. And for homeowners with heat pumps, electric cars, and other electricity-intensive items, their utility bill may reach into the $1,000s in some months. This shows them that the difference in monthly payment may not be that bad when considering all the other factors.

Emphasize resilience

While a solar battery may not save a homeowner money on energy costs, its benefits can outshine its expenses in unfortunate circumstances. If a customer lives in an area with frequent blackouts or grid failures, a solar + storage system can keep their home electrified, which is a potentially life-saving feature that is tough to put a price on.

“As we saw in Texas in 2021, and still see in California, resilience and reliability is a lot of the motivation [to go solar] in some areas,” Gilroy says.

The added benefit is that solar + storage represent larger deal sizes than solar alone.

Learn more about how to position storage in your pitch with the Pocket Guide to Selling Storage.

Focus on lifetime value

All-in-all, when you consider its benefits — including increasing home value, utility bill savings, tax benefits, resilience, and more — it’s hard to argue that solar is anything but a solid investment.

With a solar system replacing grid electricity expenses, cost must always be valued against the decades of monthly payments that a homeowner would otherwise pay the utility without a PV system. Even with high interest rates, the break-even point can come quickly, and after that the homeowner is in the black for years to come.

Solar salespeople can drive this point home with the customer by showing year-by-year returns, and contrasting monthly payments with and without solar. (Sales Mode can help.)

Learn more solar financing strategies

This just scratches the surface of what installers can do to sell solar in these uncertain times. Watch the entire panel discussion to get these financing experts’ thoughts on other ways to sell solar, unique financing options, and even thoughts on dealer fees.

Then check out our Sales Mode YouTube series to get step-by-step information on how to customize your proposals to fit each customer’s needs.

If you have specific questions about your business, schedule a no-pressure, customized demo.

Featured image by rupixen.com.